TELUS: Gaslighting Investors Since 2016

TELUS has been increasing dividends for years but now has paused this growth. We look at the dividend coverage and tell you why you should not buy.

It is hard to understand why companies like TELUS insist on destroying their equity value to create an illusion of sustainable dividend growth. We saw that a few years back with BCE where they continuously raised the dividend, even though their own "adjusted earnings" were nowhere in the ballpark of that number. In fact, had they stopped raising the dividend in 2020, and heaven knows they could use the pandemic as an excuse, they wouldn't need to cut. TELUS is the same model, but only worse.

They have not covered the dividend in any of the last 4 years. But you can note below the multitude of increases, which they colorfully describe as rewarding shareholders.

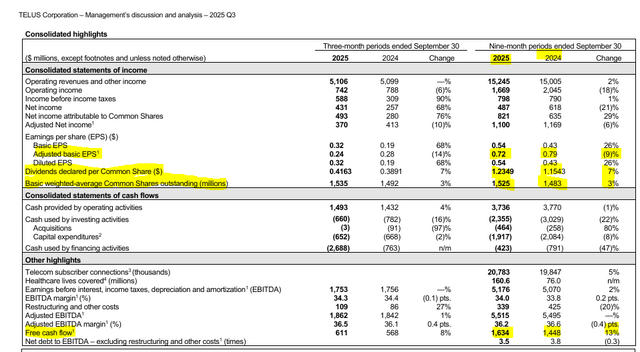

Now let's look at their latest numbers from Q3-2025, keeping in mind the dividends above.

Their adjusted EPS of 72 cents a share in the first 9 months of the year falls painfully short of the dividend of $1.2349 (yes that actually goes to 4 digits, and only TELUS knows why). 72 cents does not even cover the dividend from Q1-Q3 of 2022. In fact, you have to go to 2016 to find a dividend that is covered by current adjusted earnings.

Now some might argue it is all about the free cash flow and not the adjusted earnings. We get that and we can look at that. But before that, please note that this is not exactly oil and gas exploration companies. Free cash flow is important, but the adjusted EPS was a number designed by these guys to actually show how well their dividend was covered (in the past).

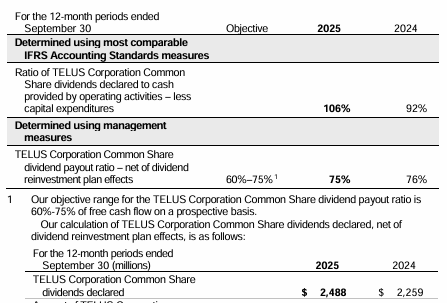

The dividends paid comes in close to $1.9 billion while the free cash blow is close to $1.6 billion. The gap is even more massive when you consider that TELUS wants to get this ratio down to 75%. Now, their 75% is net of dividend reinvestment. As in, they don't count dilution.

Of course that worked while the price of TELUS was irrationally high. With the recent collapse in stock price, the DRIP cost is now quite heavy.

Telus Corp. is pausing its dividend growth as part of an effort to reduce its leverage, an abrupt change from its previous payout plans after investors and analysts questioned the company’s ability to keep increasing dividends while meeting debt-reduction targets.

Telus said it will not increase its dividend and keep its quarterly payout at its current level until its share price “reflects growth prospects,” the telecom company said Wednesday.

The pause represents an about-face from just two weeks ago, when the company insisted that it would continue with plans to grow its dividend.

On Nov. 20, Telus chief financial officer Doug French told The Globe and Mail that management did not expect changes to the dividend-growth plan, “and management does not plan to change that, as nothing has changed in our operations.”

TELUS has also finished pulling some of its primary levers to reduce its debt. The sale of assets and hybrid issuance got debt to EBITDA down to 3.5X. Further improvement will be tough. The company is keeping a brave face and predicting 10% growth in its free cash flow.

In addition to the dividend pause, on Wednesday Telus also provided forward guidance on its free cash flow, saying it expects to generate $2.15-billion in free cash flow in 2025, and a minimum compound annual growth rate of 10 per cent between 2026 and 2028. Telus had $25.7-billion in long-term debt as of Sept. 30.

It also shared a more detailed timeline on removing the discount from its dividend-reinvestment plan, which it plans to do entirely by the end of 2027, and reiterated that it is continuing other deleveraging initiatives.

Source:

That again looks extremely optimistic. Their capital intensity is now down to about as low as it can get. TELUS is also projecting no recession between now and then and probably hoping the telecom wars are done soon.

Verdict

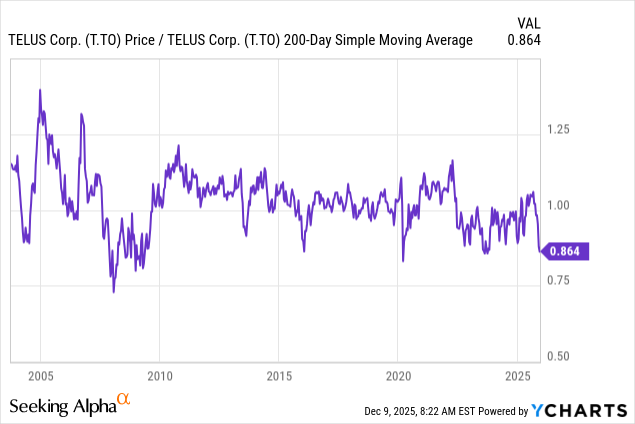

Can it rally here? Sure. It is 14% below its 200 day moving average and we have seen some big rallies from here.

The longer term outlook looks bad and if TELUS sees 2026 free cash flow aligning with our view rather than theirs, they will take an axe to that dividend. All of this would still be ok, if it was cheap. It isn't.

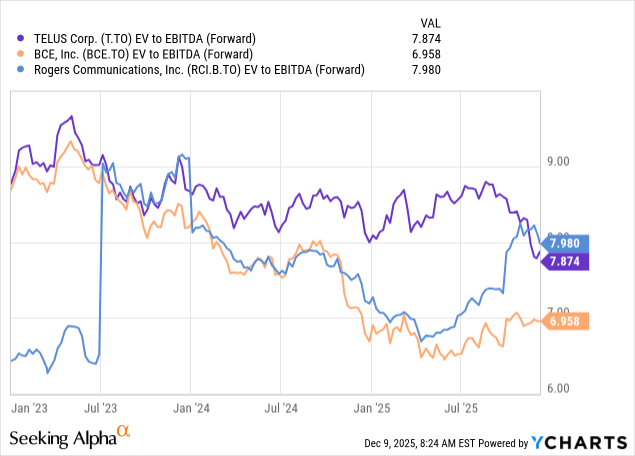

In fact, currently we wouldn't buy any of them. We will get into our defensive choices in a future article.

Trapping Value is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Trapping Value and all associates expressly disclaim all liability in respect to actions taken based on any or all of the information on this writing.

It is prohibited to copy or redistribute this report or its contents and any updates, charts or alerts to any third party under any circumstances without the permission of the author.